{kind=link}

J.G. Wentworth

If you have a structured settlement but you need ‘cash now,’ you may want to call someone else.

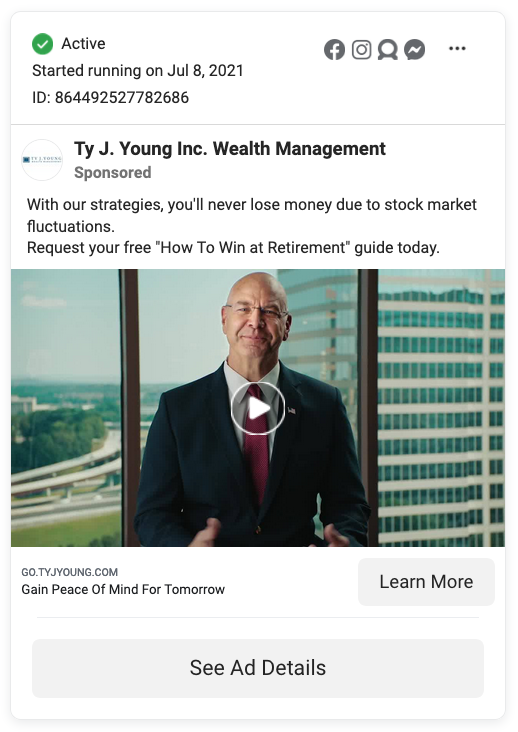

Seven years after alerting readers to important disclosures in the company’s marketing, Ty J. Young’s fine print continues to be a must-read for consumers, especially for retirees looking to grow their nest egg. Take the following claims in a Ty J. Young Facebook ad (click here to play video seen above) that started running in July and is still active as of this writing, many of which are challenged by company statements buried in a disclosure linked at the very bottom of the “wealth management” firm’s website:

Let’s tackle these in the order they appear above.

“With our strategies, you’ll never lose money due to stock market fluctuations.”

While the fixed indexed annuities that Ty J. Young sells (but doesn’t mention by name in the ad, referring only to an “investment strategy”) are designed to protect against losses when the stock market is down, you could still lose money, according to the Financial Industry Regulatory Authority (FINRA).

Fixed indexed annuities, or FIAs, are not regulated by the SEC or FINRA but rather by state insurance departments, according to Fidelity. FIAs are insurance products that base their returns on the performance of a market index, such as the S&P 500. However, FINRA warns that, “Many insurance companies only guarantee that you’ll receive 87.5 percent of the premiums you paid, plus 1 to 3 percent interest. Therefore, if you don’t receive any index-linked interest, you could lose money on your investment.” And one way you could not receive any index-linked interest, FINRA says, is if the index linked to your annuity declines. So when it comes to losing money due to the ups and downs of the stock market, Ty J. Young should never say never.

“No ridiculous fees.”

According to FINRA, the other way you could lose money on your investment is if you cancel your contract and surrender your FIA early, which Ty J. Young acknowledges in the disclosure, stating, “[A]ccounts may have a charge for surrendering the policy early or for early withdrawal.” Some might call these surrender or withdrawal charges “fees.” Some might even call them “ridiculous fees.” TINA.org could not find any information on the Ty J. Young website regarding how much these charges — or fees — may cost investors, but according to Forbes, it is typically around 7 percent of their withdrawal. In addition, if taken prior to 59 ½ years of age, an early withdrawal may also be subject to taxes and a 10 percent federal penalty.

“If you want to know more, spend five minutes with one of our advisers.”

Despite claiming to offer a proven “investment strategy,” Ty J. Young “is not an investment advisory firm,” the disclosure states. So what exactly is the role of these “advisers” that Ty J. Young would like you to spend a few minutes with? It’s simple: to sell you insurance products “on behalf of third-party insurance companies that compensate Ty J. Young,” according to the disclosure. In other words, they’re insurance salespeople.

“It’s high quality, it’s simple and it’s easy.”

If the “it” Ty J. Young is referring to as “simple” and “easy” are annuities, these investment products are notoriously complex financial instruments. In fact, according to a U.S. News & World Report article that Ty J. Young cites in the disclosure as its primary source for “[d]ata referencing annuities not losing principal due to stock market fluctuations,” annuities “are sometimes so complicated that even financial advisers have trouble understanding them.” The 2009 article, “Annuities: the Answer to a Weak Stock Market?” also states that the fees typically associated with annuities “tend to be higher than for other investment vehicles.”

FINRA has this to say about FIAs, also known as equity indexed annuities, or EIAs, and how they are anything but simple:

Although one insurance company at one time included the word “simple” in the name of its product, EIAs are anything but easy to understand. One of the most confusing features of an EIA is the method used to calculate the gain in the index to which the annuity is linked. To make matters worse, there is not one, but several different indexing methods. Because of the variety and complexity of the methods used to credit interest, investors will find it difficult to compare one EIA to another.

Which is why consumers who are thinking about investing in annuities should seek the help of an independent financial adviser and not an insurance company whose answer to the question, “I don’t like annuities, but I want my money protected. What are more options?” is to “get over the word annuity.”

TINA.org reached out to Ty J. Young for comment. Check back for updates.

Find more of our coverage on investing here.

If you have a structured settlement but you need ‘cash now,’ you may want to call someone else.

A network marketing coach doesn’t deliver on his (expensive) promises.

Precious metals seller pulls coronavirus-related radio ad following TINA.org inquiry.